Greece’s loans from the United Kingdom (1824 – 1825): Myths and truths

Nikos Apostolidis, ex NTUA Professor, member of the Advisory Board of SHP, and

Constantinos Velentzas, member of the Advisory Board of SHP

We learned recently that for the first time in the history of Greece, the yield on the 10-year Greek government bond has fallen below 1%. Something which can admittedly be considered an achievement, especially after the financial crisis of the last decade, when the return on the ten-year bonds reached the unbelievable level of 36.5%.

Coincidentally, this reminds us of the famous “loans of England” or loans of the independence, which were the first state loans concluded by Greece before it was even formally recognized as a free state.

According to the literature of the 20th and 21st centuries, many academic, journalistic and political circles refer to these loans as “burdensome” or even “robbery”, claiming that they constitute an example of exploitation of a poor country by foreign bankers, and generally of the economic exploitation of Greece by “foreigners”.

One would wonder whether these loans that Greece received from the UK, did constitute indeed a “ruthless exploitation” of the country, and whether the representatives of Greece were so foolish or incapable to agree to the terms of these loans.

Let’s examine the details of these loans first.

There were two loans.

A. The first loan was concluded in 1824 and it had the following characteristics:

Nominal loan amount: £ 800,000.

Underwriters: Loughnan Sons και Ο’Brien

5% interest rate – 1% annual ammortization rate (both on the nominal amount of the loan).

Duration 36 years.

Various commissions, guarantees, etc.

The amount disbursed was £ 472,000 or 59% of the nominal amount.

The loan was negotiated from the Greek side by I. Orlandos and Andr. Louriotis.

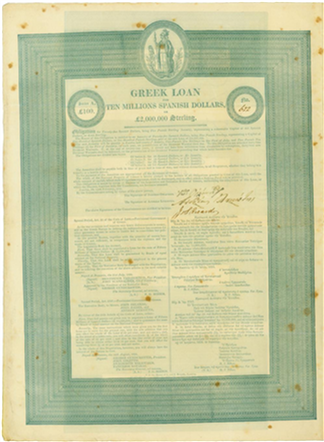

B. The second loan was concluded in 1825, and it had the following characteristics:

Nominal loan amount: £ 2,000,000.

Underwriters: Ricardo brothers

5% interest rate – 1% annual amortization rate (both on the nominal amount of the loan).

Duration 36 years.

Various commissions, guarantees, etc.

The amount disbursed was £ 1,100,000 or 55.5% of the nominal amount.

The bond of the second loan, SHP Collection.

The second loan contract also provided for a portion of the above amount to be used to pay off partially the first loan, with a total value of £ 250,000, in order to support their market value in the secondary market.

Both loans were in the form of bond issues, and in both cases the first two years’ interest payments were prepaid.

We will try to reformulate the description of the terms of these loans, in accordance with what is currently the case with the current Greek government bond loans and the terminology used today.

Let’s start with the ammortization rate.

In order to repay the capital, both contracts provided for the payment of 1% of the nominal capital annually for 36 years (the duration of the loan contracts). Of course, the sum of all these instalments amounts to only 36% of the capital. However if (theoretically) those periodic payments were deposited each year into an interest-bearing account with a relatively low, thus safe, interest rate (equal in the present case to 5%), this deposit would reach 100% of the capital at the end of 36 years.

This method of calculating the final value of a recurring payment to an account (sinking fund) of an amount X during Y years, where the amount deposited is compounded annually at a safe interest rate, has always been used and of course it applies even today. The only difference is that nowadays the safe rate (something like the interest rate of the Bundesbank or the US bonds) is about 3% or less, whereas at the time of the two loans, the safe rate was apparently 5%.

This means that the level of borrowing rates at that time, which of course fluctuated, depending on the risk of each investment, were in general almost double than those of today’s interest rates.

What may confound present-day readers is the fact that the borrowers (i.e. the revolutionary Greek government) received only a fraction of the nominal loan capital.

What was the rationale for this cut? Why, for example, in the case of the first loan, instead of cashing £ 800,000 (which was the nominal amount of the loan), Greece received only £ 472,000, or 59%?

Many think that the difference of £ 328.000 was unduly withheld by extortion and accordingly that the loan was pure “robbery”.

Were these loans indeed onerous, and did the uprising Greeks fall victims to the foreign Shylocks (like the Merchant of Venice)?

Of course not. The terms of the loan simply had to be adjusted according to the risk that loan presented.

Nowadays, the terms of a loan are adjusted according to the risk it presents, through the interest rate. The higher the risk, and the longer the repayment period, the higher the borrowing rate agreed.

Those years, however, it seems that the markets were following a different practice:

The loan contract provided for a standard interest rate (and in particular the market standard “safe” interest rate of 5%) and the adjustment of the lending terms, depending on the risk, was achieved using the method of purchasing the bonds at a price below the nominal rate. This practice is used partially even today.

In other words, this is exactly what also happens today in the secondary bond market, and the interest rate that the creditor received was what is called today the “yield” of the bond.

In effect, the real interest rate paid by the Greek state for the first loan was not the nominal 5%, but about 8.47%, i.e. 5 / 0.59.

Another small correction is needed:

Under the terms of the loans, the Greek state was paying annually 1% of the nominal amount of the loan for the amortization of the capital, while it should actually pay only 0.59% to repay the amount it actually received as a loan. To account for that, we may add this additional charge, which amounts to 0.70% of the real capital, to the interest rate of 8.47% mentioned above, resulting in a real interest rate of 9.17%, which was finally to be paid by the Greek state.

So much, as far as the first loan is concerned.

In the case of the second loan, the data are a little bit different and the real interest rate, which arises from an analysis similar to the one above, is 9.80%.

In conclusion, using present-day terms to describe the two loans, we may state that:

– The first loan was a 36-year bond issue of a total value of £ 472,000 with an interest rate of 9.17%.

It was not in reality a loan of £ 800,000, as many people believe. These people mistakenly believe that the (theoretical) difference of £ 328,000 was unduly withheld by the lenders.

– The second loan was also a 36-year bond issue of a total value of £ 1,100,000 with an interest rate of 9.80%.

It was neither in reality a loan of a value of £ 2,000,000, as the same people believe and again in this case the same as above applies to the theoretical difference of £ 900.000.

The terms of these loans, and especially the real interest rate, as calculated above, can certainly not be viewed as “robbery” at all. Especially if we keep in mind the following:

(a) the guarantees that the borrowers could present, and in particular that :

The aspiring borrowers were not even a recognised state, but merely representatives of a “rebel nation” who had long aspired to form a state, and who, after some initial successes, had even begun to clash with each other, with the conflicts having taken over the dimensions of a civil war. At the same time it must be borne in mind that the Ottoman Empire was referring to this “rebel nation” as “terrorists”, while the Holy Alliance viewed the Greek revolution negatively and as a serious threat to peace in Europe.

(b) that the overall level of interest rates was at that time internationally, higher than what it is today, as evidenced by the fact that the “safe rate” was 5%, while today it is about half that level. Therefore, the (real) interest rate of 9.5%, which was applied to Greece, corresponds to an interest rate of 5.5% – 6% with today’s standards. These terms are very favorable, at least in present day terms, let alone when it comes to 36-year bonds.

Moreover, the best proof that the terms of these loans were not onerous, but rather the opposite, is the following: one of the conditions of the second loan was to repay partially the first loan for a total nominal value of £ 250,000, as mentioned above.

This was done, and the redemption price was £ 113,200 at first stage, i.e. £ 45.3 for each £ 100 bond.

Regardless of whether this repurchase was advisable or not, we note that one year after its issuance, the price of the first loan on the free (or secondary) market had fallen from £ 59 to £ 45.4 (i.e. they were depreciated by 23%) and respectively, the bond yield went from 9.5% up to 11.9%.

So the “markets” had judged that the Greek bonds were overvalued, and that their real value, in line with the risk these bonds represented, was £ 45.4 rather than £ 59.

Therefore, it was the lenders of the first loan (that is the original buyers of the bonds) who had suffered a loss, and not the borrowers. We should also not forget that the real lenders were not some “bad” bankers, who were reasonably eager to earn a commission, but the bond holders who were mainly philhellenes (and most of them simple citizens), who wanted to help the revolted Greeks and to honor the memory and struggle of Lord Byron.

Lord Byron. Portrait. 19nth century. Oil on canvas. Collection SHP.

It is also worth noting that all the loans which were agreed by Latin American countries with English banks between 1822 and 1825, had a structure similar to that of the Greek loans. In general, if one takes into account all the facts, the terms of the loans to Greece were better. Indicatively, all loans (with the exception of the first loan of Mexico) had an initial interest rate of 6%, instead of the 5% that Greece had, while important commissions were paid.

For example, the terms of the first loan of £ 3,200,000 that Mexico received from Bank B.A. Goldsmith & Co, in 1824, were as follows. The price to buy a £ 100 bond was £ 58. The interest rate was 5%. The sale raised £ 1,850,000. However, commission of £ 750,000 were deducted. So Mexico finally got £ 1,100,000. The comparison with the terms of the Greek loan is straightforward. It is reminded that after a revolution which began in 1810, Mexico was already an independent state as of 24 August 1821.

The final conclusion is that the famous “English loans” were not robbery at all, and those who negotiated them were neither traitors nor fools. Actually, it seems that they were assisted by worthy financial advisers.

It is likely that the subsequent management of the loans was not appropriate, and it seems that several lapses have occurred, but the loans themselves were made on very reasonable terms, given all the parameters.

The problem arising from these loans was not their terms and conditions, which were not harsh at all, but the inability of the Greek state, first to use the funds optimally in favour of their struggle, and then to serve them during the years that followed, even with these objectively favorable terms.

However, it is worth noting some other parameters related to these loans. In addition to the financial aspects, these loans constituted the strongest political acts of official recognition of the revolted Greeks and the prospect of establishing an independent Greek state in the future.

The loans were made possible when the great British politician and Philhellene George Canning took the office of Foreign Affairs Minister in the United Kingdom.

Portrait of George Canning, by Thomas Lawrence, SHP Collection.

Order of the Redeemer, the medal awarded by King Othon in 1838, to the son of George Canning, Charles John Canning, SHP Collection.

Canning drastically changed the policy of his predecessor, Castlereagh. He recognized Greece as a country in war and turned on the green light for the City of London to issue loans in favour of Greece.

Gazette de France 10/3/1827. “George Canning addressed a new formal note to the Sultan for the pacification of Greece. He requested the immediate cessation of hostilities at land and sea and negotiations for a diplomatic solution in the Greek problem. It seemed that England and Russia would do anything to stop the war”. SHP Collection.

In any event, even if the Greeks had made the best use of their loans, history has shown that the liberation of Greece needed a major naval battle in Navarino.

Thomas Whitcombe circle, the Battle of Navarino, 20 October 1827, SHP Collection.

This battle involved 29 of the best ships of the three allies with the most experienced personnel aboard, under the command of the great British admiral Codrington, who crashed the Turkish-Egyptian fleet of 90 ships.

Admiral Codrington, SHP Collection.

In addition, in order to persuade Ibrahim Pascha to leave Greece, it took another 10 months and the presence of a regular army of 15,000 men under General Maison, and at the same time, continuous negotiations between Codrington and the Egyptians to reach a final agreement only in July 1828.

Has anyone ever calculated the value of this support that Greece received from its allies, and firstly from the United Kingdom? How many more loans would Greece have to receive, and which blood tax would Greeks have to pay on their own to gain their freedom?

If all of this is taken into account, then we can conclude that these loans were almost gratuitous, and that the help and support that Greece eventually received was then, as it is today, unprecedented internationally.

Greeks owe this support to the Philhellenism, to the admiration expressed by the western world to the Greek culture and heritage, which radiates through the centuries by the marbles of the Acropolis of Athens.

Bibliography:

- Ανδρεάδης Ανδρέας, Ιστορία των εθνικών δανείων, Αθήνα 1904